Personal Guarantee on a Merchant Account?

A Merchant Account Personal Guarantee is a commitment made by a business owner or merchant, promising to be personally liable for any outstanding debt

What is the FedNow Service?

FEDNOW was introduced by the United States Federal Reserves, the FedNow Service is one of the latest and most advanced real-time payment platforms. It has been rece

What is a Rolling Reserve Account?

A rolling reserve account is a financial arrangement used by merchant account processors to manage risks associated with payment processing and trans

As more and more people turn to online transactions for security and convenience, Online Banking ePayments (OBeP) have become increasingly popular in recent years. OBeP is a convenient and se

No PCI Compliance Fees

PCI Compliance refers to a set of security standards that have been created to make sure that all merchants and businesses that accept and process credit card data m

What is Merchant

Account Load Balancing?

Load balancing a merchant account allows for the dynamic division of transactions across multiple merchant accounts. With load balancing, a high volume

High Risk Merchant Account Integration Into WooCommerce

Getting A High Risk Merchant Account For WooCommerce

Deciding the payment method for your business is key to ensuring a seamless customer

Chargeback Reduction Plan For Your Business

Taking credit card payments at business while being an easy payment method could become a disaster sometimes when card users dispute payments and a charg

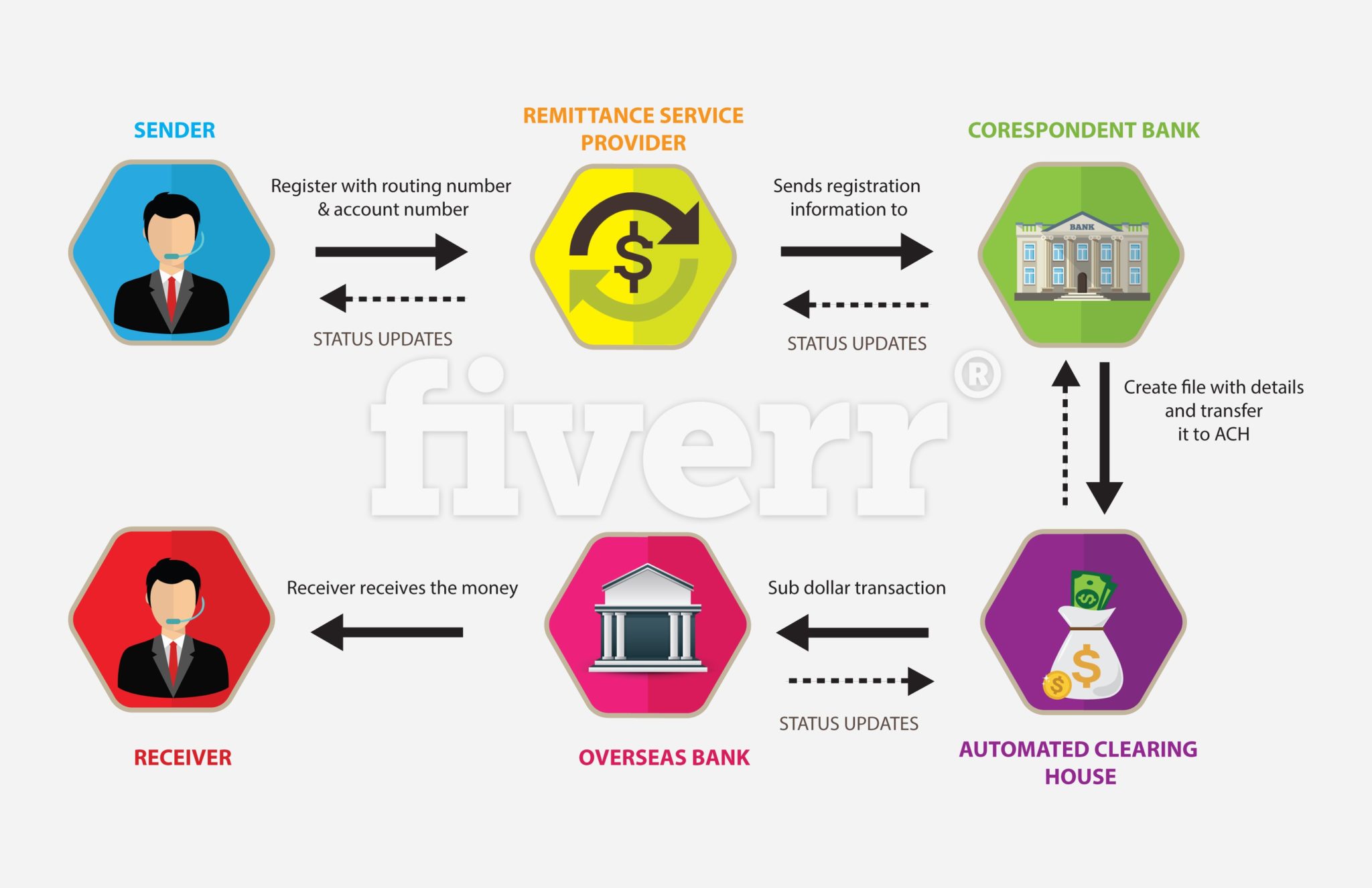

Understanding ACH Payments

In order to perfectly understand how these kinds of payments are made, it’s essential to comprehend them entirely, as well as to know what t

What Is The Dreaded TMF File

To the average person, the words “terminated merchant file” does not mean much, but for a business using merchant account services, it can mean utter ruin. Landin